Policy Uncertainty during the Shutdown: Elevated

[ad_1] Daily data from Baker, Bloom and Davis: Figure 1: EPU (blue, left scale), EPU-trade (green, right scale). Light orange is Trump

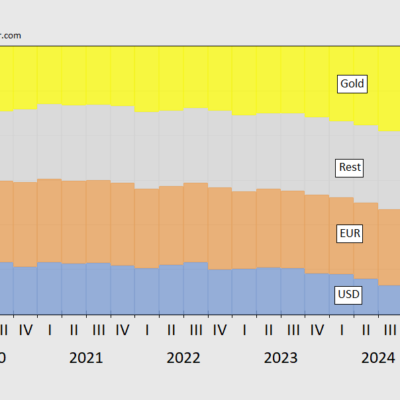

FX and Gold Reserves in Q2

[ad_1] COFER data is out for Q2. With estimated gold held by the central banks, we have this picture of reserve composition.

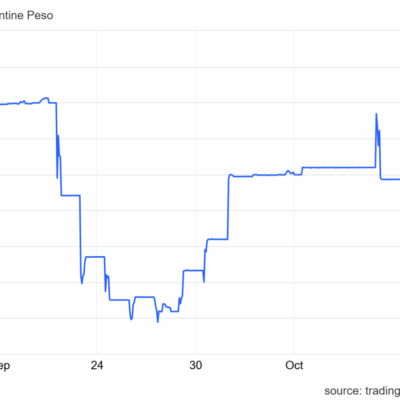

How Much Will We Lose Lending to Argentina?

[ad_1] The $20 billion swap announced by Bessent (not on US Treasury website as far as I can tell) is funded out

WSJ Survey: Below Trend Growth

[ad_1] Out today: Figure 1: GDP (bold black), WSJ mean (blue), WSJ +/- 20% bounds (gray), GDPNow of 10/7 (light blue square),

Why a Missed Release Is Sometimes Problematic

[ad_1] When the economy is growing in a steady manner, a missed release is not a problem. But when the economy is

Flying Blind, Graphically Illustrated | Econbrowser

[ad_1] Here’re key indicators followed by the NBER’s Business Cycle Dating Committee, with indications of measures already missed (purple squares) and will

On Immigration Policies and the Ag Sector

[ad_1] An assessment of how current Administration polices regarding immigration and removals are affecting the agricultural sector (October 2): Agricultural employers, who have been incentivized

Why I Think the Administration Would Be Happy to Let the October Employment Release Slip

[ad_1] Effective September 30th, some 105000 Federal workers who had signed up for the Deferred Resignation Program will be officially unemployed. The

EJ Antoni: Back to Smearing Data Sources

[ad_1] Antoni on X: The reason that UMich’s fake inflation expectation data can sometimes rise when all 3 components (R’s, D’s, and I’s) decrease is

Memo from the Midwest: Thanks, Drumpf!

[ad_1] November futures for soybeans collapse upon Trump’s announcement: Source: barchart.com . [ad_2] Source link