[ad_1]

GDPNow at essentially zero growth. Industrial production, retail sales (control) surprise downside.

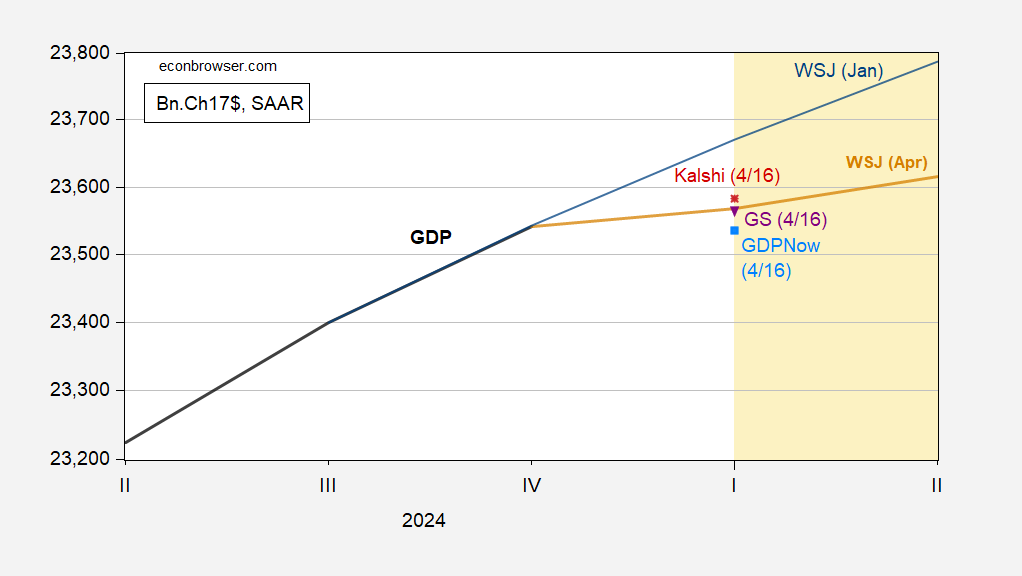

Figure 1: GDP (bold black), WSJ January survey mean (blue), WSJ April survey mean (tan), GDPNow of 4/16 (sky blue square), Goldman Sachs tracking forecast of 4/16 (inverted purple triangle), Kalshi forecast of 4/16 (red *), all in billions Ch.2017$ SAAR. Source: BEA 2024Q4 3rd release, WSJ survey.

That being said, net exports are providing an outsized negative contribution in an accounting sense to Q1 GDP (-2.86 ppts q/q AR).

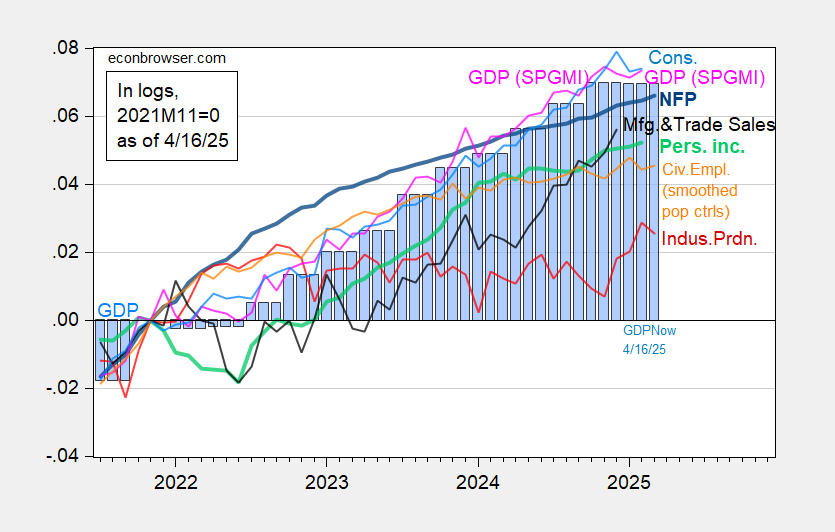

Business cycle indicators augmented today with industrial production indicate a slowdown, but we don’t yet have the critical consumption and personal income numbers for March.

Figure 2: Nonfarm Payroll incl benchmark revision employment from CES (bold blue), civilian employment using smoothed population controls, spliced to official (orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold light green), manufacturing and trade sales in Ch.2017$ (black), consumption in Ch.2017$ (light blue), and monthly GDP in Ch.2017$ (pink), GDP (blue bars), all log normalized to 2021M11=0. Source: BLS via FRED, Federal Reserve, BEA 2024Q4 3rd release, S&P Global Market Insights (nee Macroeconomic Advisers, IHS Markit) (4/1/2025 release), and author’s calculations.

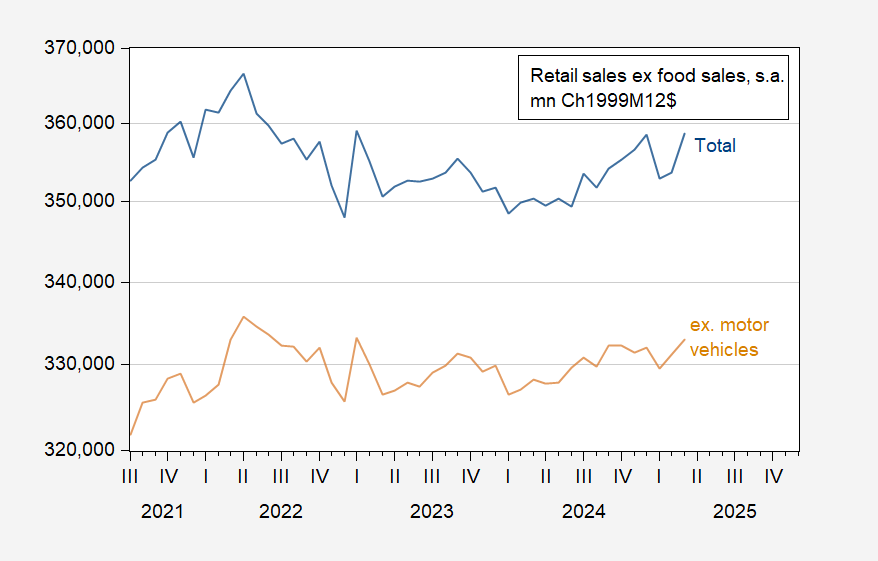

Here’s a picture of real retail sales ex-food sales, and ex-motor vehicles.

Figure 3: Total retail sales ex-food sales (blue), Retail sales ex-food sales and ex-motor vehicles (tan), mn.Ch.1999M12$, s.a. Source: BEA, BLS via FRED, and author’s calculations.

By my accounting, nominal motor vehicle sales increased 13% m/m (not annualized), while non motor vehicle sales rose 0.5%, In other words, there’s a lot of tariff jumping aimed at avoiding higher car prices.

[ad_2]

Source link