[ad_1]

That’s EJ Antoni/Heritage Foundation, writing in September 2022. A cautionary note on declaring recessions.

Furthermore, the Biden administration’s cherry-picking of data has come back to bite it, with even its selected data points now being revised to indicate a recession. And while these numbers confirm the economy shrank in the first half of the year, the rest of this year holds little promise of recovery.

Just a reminder of what data we know now about 2022H1, and what happened subsequently.

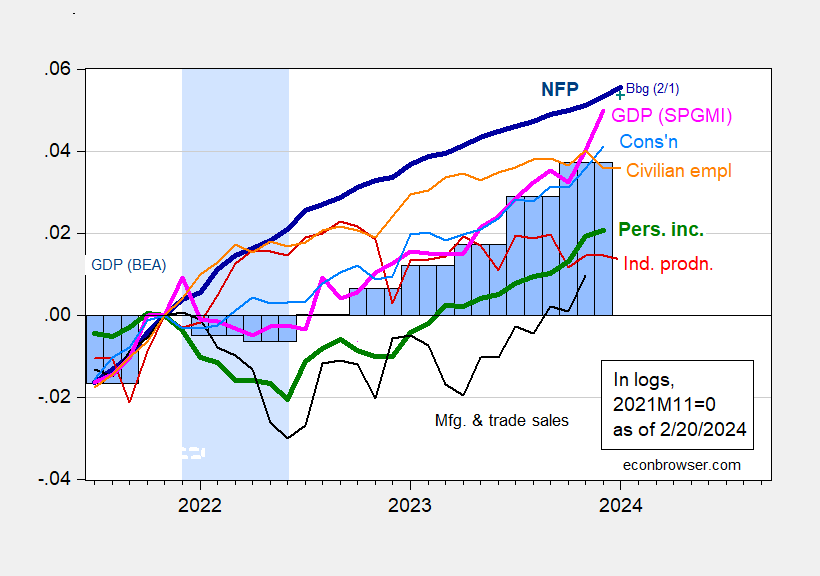

Figure 1: Nonfarm Payroll employment (bold dark blue), Bloomberg consensus of 2/1 (blue +), civilian employment (orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold green), manufacturing and trade sales in Ch.2017$ (black), consumption in Ch.2017$ (light blue), and monthly GDP in Ch.2017$ (pink), GDP, 2023Q4 advance release (blue bars), all log normalized to 2021M11=0. Hypothesized 2022H1 recession shaded light blue. Source: BEA, BLS via FRED, Federal Reserve, 2023Q4 advance release,, S&P Global Market Insights (nee Macroeconomic Advisers, IHS Markit) (2/1/2024 release), and author’s calculations.

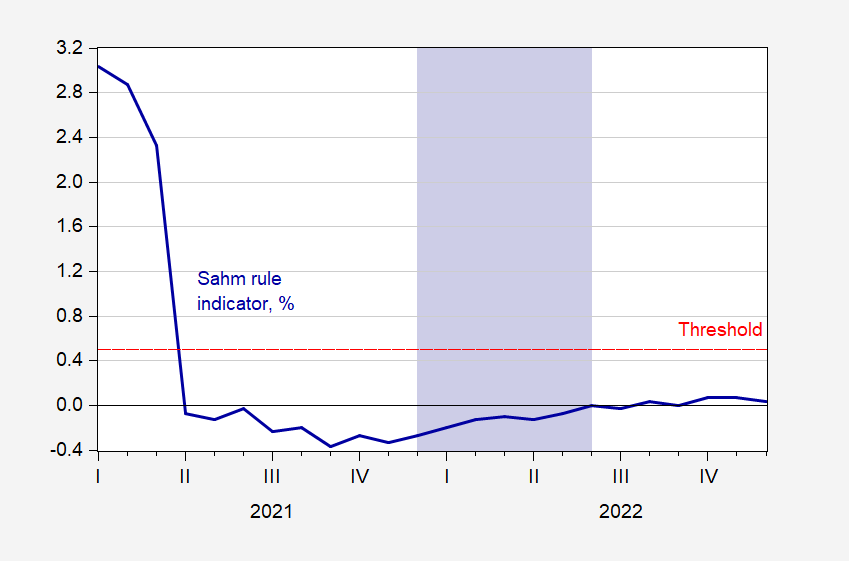

What about the Sahm rule (real time)?

Figure 2: Real time Sahm rule indicator, in % (blue). Threshold denoted by red dashed line. Putative peak-to-trough recession of 2022H1 shaded lilac. Source: FRED.

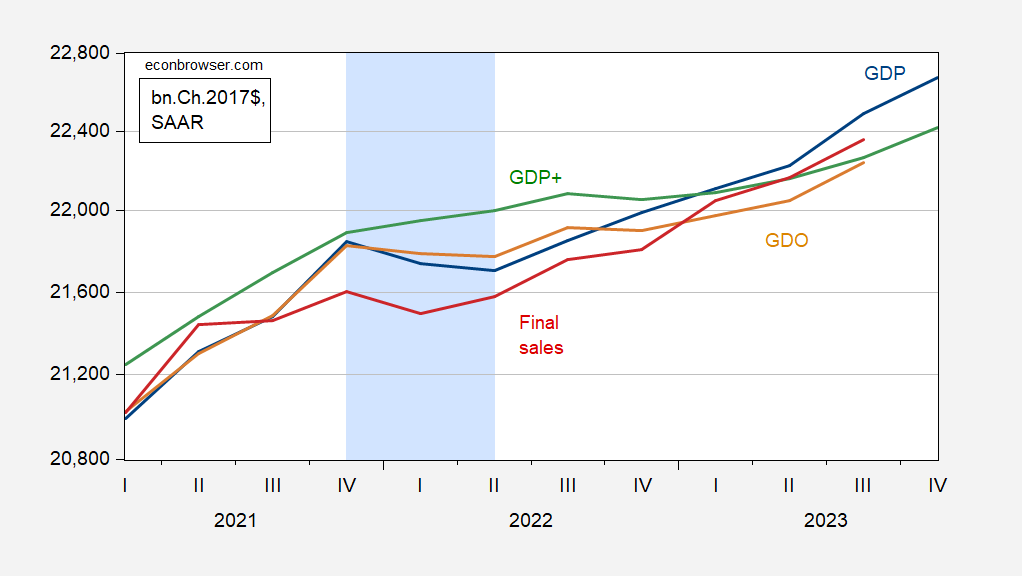

And, recalling that NBER’s BCDC doesn’t place primary reliance on GDP, here are other measures of output.

Figure 3: GDP (blue), GDO (tan), and GDP+ (green), final sales (red), all in bn.Ch.2017$ SAAR. GDP+ assumes 2019Q4 GDP+ equals GDP. Hypothesized 2022H1 recession shaded light blue. Source: BEA 2023Q4 advance estimate, Philadelphia Fed, and author’s calculations.

So, now Dr. Antoni has declared us in recession, as of several weeks ago. He might end up being right. As of yesterday, nowcasts are rising, the Lewis-Mertens-Stock Weekly Economic Index is running at 2.37%.

[ad_2]

Source link